This text is an automatic translation from Русский. It was generated by AI and may contain inaccuracies.

Read original →Metals of the Future: How Rare Earths Are Reshaping the Global Balance of Power

Rare earth elements have become the strategic resource of the 21st century. How China monopolized the REE market, why the U.S. is searching for alternatives, and what prospects Russia has with its vast rare earth reserves.

Metals of the Future: What Lies Behind the Term "Rare Earths"

Let's start with a bit of chemistry: rare earth elements (REEs) are a group of 17 metals that includes scandium, yttrium, lanthanum, and the 14 lanthanides that follow it in the periodic table (cerium, neodymium, europium, dysprosium, and others). These are mostly malleable, silvery-white conductors. Their key property is the ability to form numerous complex compounds with other metals. This is precisely what allows them to be used as "additives" that radically transform and improve the properties of alloys.

Despite their name, rare earths aren't actually all that rare in nature—they occur quite frequently, but they rarely form deposits that are convenient to mine. Typically, they're dispersed throughout the earth's crust, and their concentration in ore often doesn't exceed 100 grams per ton. Because of such low concentrations, profitable extraction is only possible as a byproduct, when REEs are recovered as a secondary material during the mining of other, more common metals.

Another important characteristic of REEs is their similar chemical properties, and this similarity makes the process of separating and purifying the elements technically complex and economically costly. Promethium stands out in particular—it has no stable isotopes and is virtually nonexistent in nature, forming only as a result of radioactive decay of uranium.

Global Rare Earth Deposits: Who Controls Strategic Resources

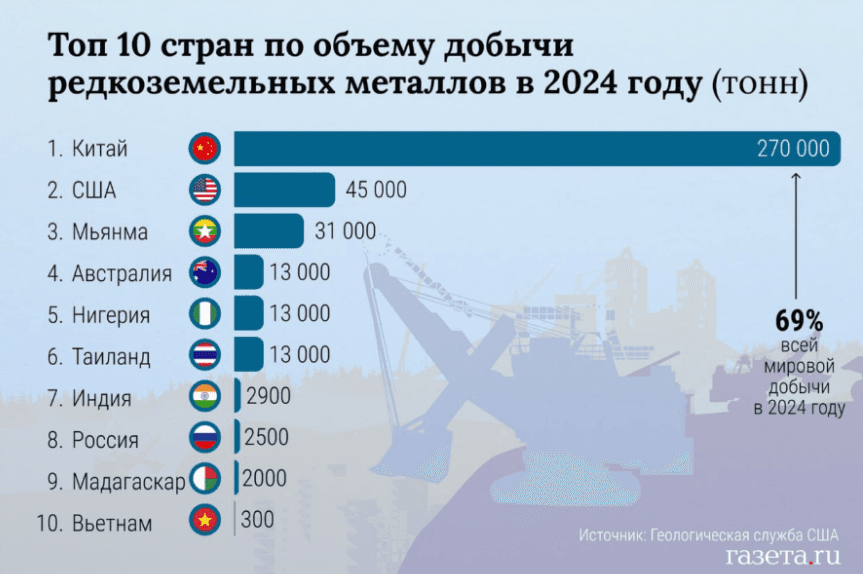

According to estimates from the U.S. Geological Survey, global reserves of rare earth metals in 2024 exceed 90 million tons. However, they're distributed extremely unevenly across the planet.

China is the absolute leader in reserves, holding nearly half of the world's resources—between 40 and 45 million tons. A significant share of deposits, around 20-25% each, is concentrated in Russia and Brazil. Estimates of Russian reserves vary dramatically across different sources: according to Russia's Ministry of Natural Resources, the country holds more than 28 million tons of rare earths, while the U.S. Geological Survey counts only 3.8 million tons of proven REE deposits. Other countries with the largest reserves include India (6.9 million tons) and Australia (5.7 million tons).

The production picture shows an even more significant imbalance. In 2024, global REE extraction totaled 393,800 tons. And here China demonstrates absolute monopoly—accounting for about 70% of all mining and over 90% of processing. The country is home to more than 200 rare earth enterprises, including around 30 mines and over 10 processing plants. Such concentration of production transforms the Middle Kingdom not just into a leader, but into a monopolist dictating terms in the global rare earths market.

China's example is unique, however, as countries with large reserves aren't always such major producers. For instance, Russia, despite possessing significant resources, currently occupies an extremely modest position in global production—less than 1%. Extracting them is economically unfeasible: promising deposits are located in hard-to-reach territories without appropriate infrastructure. This confirms that beyond the presence of deposits, developed technologies and infrastructure for their development are critically important—a factor China has been able to leverage. Internal demand for REEs is also key: in Russia's case, the domestic economy's needs for these metals remain modest so far and are estimated at approximately 2,000 tons per year. With such modest domestic demand, large-scale investments in deposit development become economically impractical, since the produced output won't be fully absorbed by the internal market, while external markets are constrained by sanctions pressure.

The New Oil: The Value of Rare Earths for the 21st Century Economy

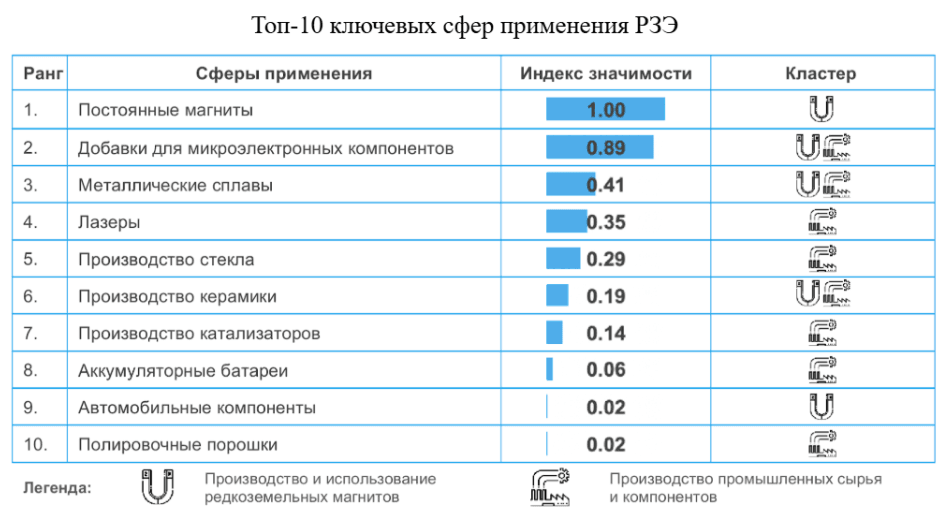

The unique properties of rare earth elements have found applications across all key high-tech sectors—from electronics to energy and defense. Their impact is particularly notable in permanent magnets based on neodymium and samarium: the former power electric vehicle motors, drones, and wind turbine generators, while the latter are used where high heat resistance and reliability are required, such as in aviation. The development of green energy and electric transport remains the primary driver of global demand for rare earth elements.

In electronics, rare earths are responsible for screen brightness and precision, the operation of optical lenses and sensors: europium and terbium are used in phosphors, yttrium in laser systems, and cerium in polishing optical glass. In the defense sector, they are essential for guidance systems, laser rangefinders, night vision devices, and satellite communications.

Control over supplies of these elements is already viewed as a matter of national security: without reliable sources and processing capabilities, mass production of electronics and creation of high-precision weaponry is impossible, while substituting rare earth elements in most critically important technologies remains economically and technologically impractical.

How rare earths became a tool of trade confrontation

The demand for rare earths in key industries has turned access to them into one of the central elements of trade rivalry between the U.S. and China. According to the U.S. Geological Survey, in 2020–2023, approximately 70% of rare earth metals and compounds imported into the U.S. came from China. A vivid confirmation of this vulnerability came in 2022, when it was discovered that one component of the F-35 fighter engine—a samarium-cobalt magnet—was manufactured in China. This prompted Washington to accelerate development of its own capabilities, but complete reorientation of the defense-industrial complex to "domestic" rare earths takes time. But the Pentagon has already taken the first step: a law was passed prohibiting the use of rare earth metals mined or manufactured in China, Russia, Iran, or North Korea starting January 1, 2027.

During Donald Trump's second term, at the height of the trade war, rare earth supplies became one of Beijing's key leverage tools. In response to Trump raising tariffs on Chinese goods to 145%, China imposed a ban on exports to the U.S. of seven rare earth metals—samarium, gadolinium, terbium, dysprosium, lutetium, scandium, and yttrium. After this, tariffs were partially reduced—to 30%.

However, the confrontation intensified again in October 2025: Beijing expanded its list of restrictions, tightening control over rare earth exports, as well as over production technologies and their foreign applications, including military purposes and semiconductor manufacturing. This was followed by sharp statements from Washington about possible countermeasures, including threats to increase tariffs to 100% and restrict exports of critical software. The outcome of the confrontation remains uncertain and will depend, among other things, on bilateral negotiations between the countries' leaders at the APEC summit in South Korea. Meanwhile, Washington isn't wasting time and is actively seeking alternatives to Chinese rare earth metals. Trump signed an agreement with Australian Prime Minister Albanese on joint investments (over $3 billion) in critical metals projects, plus the Pentagon is to invest in building a gallium processing plant in Western Australia with a capacity of 100 tons per year. Additionally, the White House is actively facilitating American company Cove Capital's access to one of the world's largest unexplored tungsten deposits in Kazakhstan. This metal is needed by the Pentagon for producing ammunition, shells, and other weaponry. Thus, Washington is seeking to reduce dependence on the dominant rare earth supplier—Beijing—and create its own supply chains for critical materials.

Russia's rare earth card

Russia possesses some of the world's largest reserves of rare earth metals: approximately 18 deposits have been officially surveyed. However, the only commercially operating deposit currently is Lovozero in Murmansk Oblast: loparite concentrate is extracted from its ores, which is then sent to Perm Krai. There, niobium, tantalum, and titanium compounds are extracted from the concentrate. The resulting carbonate containing 16 rare earth elements is exported to China, since Russia currently lacks large-scale facilities for deep processing and manufacturing high value-added semi-finished products.

The largest—Tomtor—is located in Yakutia and is considered one of the world's "richest" deposits in terms of rare earth element concentrations. Projected resources are estimated at 154 million tons of ore with a record content of rare earth element oxides—up to 10%, including strategically important niobium, terbium, yttrium, and scandium. According to estimates of Nikolai Kruk, director of the Institute of Geology and Mineralogy of the Siberian Branch of the Russian Academy of Sciences, Tomtor's rare earth reserves "will last for hundreds of years even with explosive growth in their consumption." However, Tomtor's development has been repeatedly delayed due to the lack of processing technologies, complex and expensive logistics (the ore was planned to be processed in Krasnokamensk in Zabaykalsky Krai, located 5,000 km from the deposit), as well as protests from local residents concerned about the high radioactivity of the ores. In 2024, the president publicly criticized the slowdown in work, and in May 2025, Rosneft gained control over the project operator—Vostok Engineering—signaling a strengthening of the state's role in this strategic sector and an ambition to take the country's rare earth metal development to a new level.

In parallel, the Ministry of Industry and Trade announced preparations to launch major investment projects for rare earth elements in Murmansk Oblast, Irkutsk Oblast, and Yakutia. The strategic goal is to scale up rare earth production to 50,000 tons by 2030, which would significantly reduce import dependence (from 75% to 45%). Prospects for international cooperation, particularly with the United States—joint projects with which were discussed in early 2025—remain murky against the backdrop of tightening sanctions pressure. Under these conditions, the success of Russia's rare earth strategy will depend on its ability to create a closed production cycle—from extraction to high-tech products—as well as ensure sufficient domestic demand.